1.Introduction

If you are selling privately in Ontario, you will hear two terms early in the process: CMA and appraisal.

They both relate to what your home may be worth, but they are not interchangeable. A comparative market analysis, usually called a CMA, helps you choose a sensible listing price. An appraisal is a formal opinion of value prepared for a specific purpose, often because a buyer’s lender needs it before approving their mortgage.

Knowing the difference matters. It helps you avoid one of the most expensive FSBO mistakes: treating a rough online estimate, a neighbour’s sale, or a lender’s appraisal as the only number that should determine your asking price.

2.Table of Contents

- CMA vs appraisal at a glance

- What a CMA is and how it helps private sellers

- What a home appraisal is and why lenders use it

- The biggest differences between a CMA and appraisal

- When an Ontario private seller should use a CMA

- When it makes sense to pay for an appraisal

- What happens when the buyer’s appraisal comes in low

- How to price a private sale using both market data and judgement

- Documents that improve your pricing file

- How Realkit helps keep your pricing and sale information organized

- Frequently Asked Questions

- Conclusion

- Sources

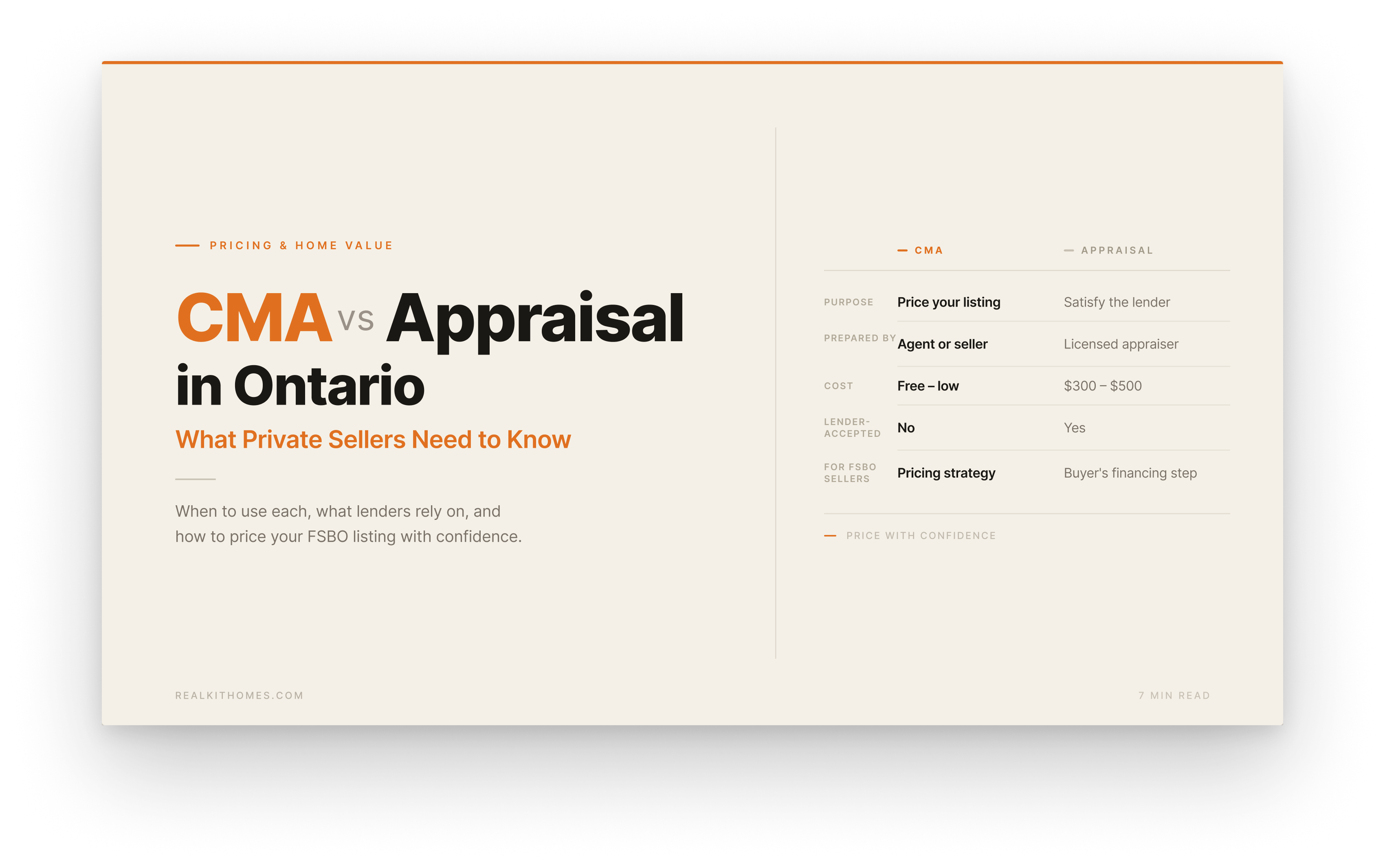

3.CMA vs Appraisal at a Glance

A CMA is a pricing tool. An appraisal is a formal valuation report.

A comparative market analysis, or CMA, helps you decide how to position your home for sale. It looks at recent comparable sales, current listings competing for the same buyers, homes that did not sell, and the details that make your property different. Its purpose is to help you choose a reasonable asking-price range and prepare for buyer questions.

An appraisal is a more formal opinion of value prepared by an independent appraiser for a defined purpose. In an Ontario home sale, the most common example is a buyer’s lender ordering an appraisal before finalizing mortgage financing. Appraisals may also be used for refinancing, estate matters, separation, tax issues, or other situations where an independent valuation is required.

The most important difference is what each one is designed to do. A CMA helps you decide how to list and compete in the live market. An appraisal helps a lender or another party assess the property’s value for a specific financial or legal purpose.

A CMA is generally prepared by a real estate agent or built by a careful seller using comparable market data. It is flexible in format and can include active listings, price reductions, local buyer behaviour, and other details that affect how your home should be marketed.

An appraisal is prepared by an independent professional appraiser. Appraisers provide valuation services for property owners, lenders, and other clients, and mortgage professionals may rely on their reports when assessing a property for financing.

There is also a practical cost difference. A CMA is often offered at no direct charge when an agent is trying to earn a listing, although a private seller can also build a pricing file themselves. An appraisal is normally a paid report, and the price can rise for rural, unique, high-value, or more complicated properties. Ontario examples commonly place straightforward residential appraisals in the several-hundred-dollar range.

4.What a CMA Is and How It Helps Private Sellers

CMA means comparative market analysis

A comparative market analysis looks at properties similar to yours and asks a practical question:

“If buyers have recently paid these amounts for similar homes nearby, where should this home be positioned today?”

A strong Ontario CMA normally considers:

- Recent sold properties that are genuinely comparable

- Current active listings competing for the same buyers

- Listings that were cancelled, expired, or repeatedly price-reduced

- Property type, lot size, layout, bedroom count, parking, condition, and updates

- Location details such as a busy road, school zone, transit access, ravine lot, or downtown proximity

- Current market conditions in your local area

The word “comparative” is important. You are not looking for the highest sale within a broad postal code. You are looking for homes that a buyer would reasonably put beside yours when deciding where to spend their money. A CMA is commonly used to establish a practical starting point for a listing or negotiation because it compares features and nearby market activity.

A CMA gives you a range, not a guarantee

A good CMA should not produce one magical, exact number.

Instead, it should help you identify:

- A conservative range where the home may attract attention quickly

- A realistic target range based on the strongest comparable sales

- A stretch range that may be difficult to justify unless your home has meaningful advantages

For example, suppose you own a three-bedroom semi in Hamilton. Recent nearby semi-detached sales might range from $760,000 to $835,000, but the higher-end homes have renovated kitchens, finished basements, and deeper lots.

If your home has a newer roof and good parking but an original kitchen, listing at the top of the range simply because one nearby home sold there is risky. A CMA helps you adjust for the real differences buyers will notice.

Private sellers can build a better CMA than they think

You do not need to be a real estate professional to think like a careful seller.

Start by creating a short comparison sheet with:

- Your address and basic property facts

- Three to six recent sold comparables

- Three to six current competing listings

- Notes on differences that matter

- Your planned asking price and the reason for it

Do not compare a renovated detached home on a quiet crescent with an older semi on a main road just because they have the same number of bedrooms. Buyers will not see them as equal, so neither should you.

If your property is unusual, high-value, rural, recently rebuilt, or difficult to compare, a professional appraisal may be worth considering before you list.

5.What a Home Appraisal Is and Why Lenders Use It

An appraisal is a formal valuation for a defined purpose

A home appraisal is prepared by an independent appraiser. It is more structured than a CMA and is normally created for a specific client and purpose.

In a financed Ontario purchase, the buyer’s lender may request an appraisal to help assess the property as security for the mortgage. The lender decides whether it needs an appraisal, what type of report it requires, and how the report will be used in the mortgage file. Mortgage professionals rely on independent appraisers when they need support for credit and lending decisions.

The person ordering the report is often the lender, lender’s agent, or mortgage professional, not the seller.

What an appraiser may review

The scope depends on the assignment, but an appraiser may assess:

- Property type, size, layout, and condition

- Location, neighbourhood, access, and marketability

- Recent comparable sales

- Renovations, additions, deficiencies, and unusual features

- Exterior and interior characteristics

- Relevant market conditions around the valuation date

For mortgage work, lender requirements can be detailed. They may require recent comparable sales, interior and exterior photos, notes about deficiencies, and confirmation of key property features and services.

An appraiser is not there to help either side “win” a negotiation. Their role is to provide an independent opinion within the scope of their assignment.

An appraisal is not the same as your MPAC assessment

Ontario homeowners sometimes confuse an appraisal with their property tax assessment.

They are different:

- Your MPAC current value assessment is used for municipal and education property tax purposes.

- A market appraisal is an opinion of value for a specific assignment and date.

- Your home’s sale price is the amount a willing buyer and seller actually agree to in the market.

Do not use your MPAC assessment as your only pricing tool. It may be useful background information, but it is not a current pricing plan for a private sale.

6.The Biggest Differences Between a CMA and Appraisal

Purpose: marketing versus formal valuation

A CMA helps you answer, “How should I list this home so buyers take it seriously?”

An appraisal helps answer, “What is this property worth for the purpose of this specific lending, financial, or legal assignment?”

That distinction becomes important after you accept an offer. You may price your home using a well-supported CMA, but a buyer’s lender may still order an appraisal before final mortgage approval.

Who prepares it: market professional versus independent appraiser

A CMA is generally prepared by an agent or brokerage as part of a pricing discussion. Some private sellers also build their own version using available sales and listing information.

An appraisal is prepared by an independent appraiser with professional valuation training and qualifications. The Appraisal Institute of Canada identifies its members as professionals providing independent appraisal services.

Scope: flexible comparison versus structured report

A CMA can vary widely in quality.

One CMA might simply list recent sales. Another might carefully adjust for lot size, renovations, basement finish, parking, school catchment, condo fees, and active competition.

An appraisal follows a more defined assignment scope. This can make it more useful for formal purposes, but it does not mean it is automatically the best tool for setting your day-one asking price.

A seller needs to understand buyer behaviour. That is why current listings, recent price reductions, and local demand can be just as important to your listing strategy as the sold comparables in an appraisal report.

Cost: usually free versus usually paid

A CMA is often offered without a direct fee as part of an agent’s effort to earn a listing. A private seller can also obtain market data through a flat-fee MLS provider, a paid data service, or a real estate professional who offers a pricing consultation.

An appraisal is usually paid for. Pricing can vary based on complexity, property type, location, urgency, and the purpose of the report. Ontario examples commonly place residential appraisal costs in the several-hundred-dollar range, with more complex properties costing more.

Do not choose an appraisal simply because it feels more official. Choose it when you need the level of independence and detail it provides.

7.When an Ontario Private Seller Should Use a CMA

Use a CMA before you choose an asking price

For most private sellers, a CMA is the first valuation tool to use.

It helps you decide:

- Whether your expected price is grounded in the market

- Whether you should list at a sharp price to attract early interest

- Whether your home has enough advantages to justify a premium

- How to explain your price if buyers or buyer agents challenge it

The best time to build your CMA is before photos, marketing, and showings. It is much easier to make a calm pricing decision before you have put emotional energy into the listing.

Refresh it when your listing is not getting traction

A CMA is not “done forever” on listing day.

If your home has been listed privately for a few weeks and you are seeing:

- Very few inquiries

- Lots of saves but no showing requests

- Showings with repeated comments about price

- Comparable homes selling while yours is still available

Refresh the CMA.

Look at new listings and recent sales. Ask whether you are now competing against better-value homes. Review whether the issue is price, photos, presentation, buyer access, or exposure.

Longer days on market can change a buyer’s perception, which is why pricing is one of the main factors that affects a private sale timeline.

Use it to prepare for buyer-agent conversations

If an agent brings a buyer to your private listing, they may arrive with their own comparables.

You do not need to argue about every sale. But you should be ready to explain:

- Why your home is priced where it is

- Which updates or features matter

- How it compares with nearby active listings

- Whether there is room to negotiate and what matters beyond price, such as closing date or conditions

Being prepared is not about “winning” a debate. It keeps you from reacting to the first confident-sounding number an agent presents.

8.When It Makes Sense to Pay for an Appraisal

Your home is difficult to compare

An appraisal may be useful before listing if your home does not have easy comparables.

Examples include:

- A rural home with acreage, a well, septic system, outbuildings, or multiple structures

- A waterfront or vacation property

- A custom-built home

- A property with a legal secondary suite or unusual income potential

- A house that has been extensively renovated or rebuilt

- A very high-value home with few nearby sales

- A mixed-use or unusual zoning situation

In these cases, a standard CMA may provide a wide range rather than a confident pricing position.

You need a formal opinion for a non-sale purpose

You may need an appraisal if you are dealing with:

- Refinancing or a home equity line of credit

- Estate planning or estate administration

- Separation or division of property

- Tax, insurance, or legal matters

- A dispute where a formal value opinion is needed

This is a different situation from normal listing preparation. For these matters, speak with the professional involved in your file and ask what type of appraisal or valuation they require.

You want an independent check before a high-stakes decision

Some private sellers choose to pay for an appraisal when the possible pricing error feels too large.

For example, if you are deciding whether to list a unique Ottawa home at $1.15 million or $1.35 million, a few hundred dollars for independent valuation may be worth it. The report will not decide your asking price for you, but it can make your decision more grounded.

An appraisal can also help if family members disagree about value. It creates an independent reference point, which can make a difficult conversation less emotional.

9.What Happens When the Buyer’s Appraisal Comes In Low

A low appraisal can create a financing gap

Suppose you accept a private-sale offer for $900,000. The buyer is financing the purchase, and their lender orders an appraisal. If the appraised value comes in lower than the agreed price, the lender may base its loan on the lower amount.

The buyer may then need to:

- Bring more cash to closing

- Seek a different lender or mortgage structure

- Renegotiate the price

- Rely on the wording of their financing condition and their ability to satisfy it

The result depends on the purchase agreement, the buyer’s financing, and the parties’ choices. This is a good time to speak with your lawyer before agreeing to any change.

Do not assume the appraisal is the final word

A lender’s appraisal matters a great deal to the buyer’s financing, but it is not automatically the price you must accept.

A low appraisal may reflect:

- A quickly changing market

- Limited recent comparables

- A feature the appraiser did not weigh as heavily as you expected

- A property that sold above the range supported by the lender’s preferred comparables

Your practical next step is to ask for clarity through the buyer’s side, discuss your options with your lawyer, and decide whether the buyer can bridge the difference, whether a renegotiation makes sense, or whether you should hold your position.

Do not make rushed promises by text or phone. If the deal terms are changing, get legal guidance and make sure the written documents reflect the final agreement.

10.How to Price a Private Sale Using Both Market Data and Judgement

Start with sold comparables

Begin with three to six recent sales that are as close as possible in:

- Neighbourhood

- Property type

- Size and layout

- Lot characteristics

- Parking

- Condition and renovations

- Building age, where relevant

For a condo, compare similar units in the same building first where possible, then nearby buildings with similar fees, amenities, age, and location. A two-bedroom unit with $850 monthly fees is not directly comparable with a similar-sized unit carrying $500 monthly fees.

Check active competition before setting the price

Sold data tells you what buyers accepted in the past. Active listings show what buyers can choose today.

Before listing, ask:

- What will buyers see immediately after viewing my home?

- Is a similar home listed for less?

- Does a competing home have better photos, a larger yard, or newer finishes?

- How many days have competing homes been listed?

- Have they already reduced their price?

This is one of the details generic pricing advice often misses. You are not pricing against last month’s sold homes alone. You are competing against the homes a buyer can book this weekend.

Decide what your list price is meant to do

Your asking price should have a job.

It may be intended to:

- Attract a wide group of buyers quickly

- Test a premium for an unusual feature

- Match a clear group of recently sold comparables

- Leave a realistic amount of negotiation room

- Meet a timing goal before buying another home

Avoid listing high simply because you can always reduce later. Early interest is usually your strongest interest. A private seller who starts too high may lose the buyers most likely to act quickly, then spend weeks chasing the market down.

For a full look at how poor pricing affects your final result, see common FSBO mistakes that quietly cost sellers money.

Keep a written pricing file

Create a folder that includes:

- Your comparison sheet

- Links or printouts for comparable homes

- Photos and notes on upgrades

- Property tax and utility details

- Renovation invoices, permits, warranties, and survey documents if available

- A record of buyer feedback once the listing goes live

This is useful for your own decision-making and can help you respond consistently when buyers ask why the home is priced the way it is.

11.Documents That Improve Your Pricing File

Buyers often judge value based on uncertainty.

The more clear information you can provide, the easier it is for a serious buyer to understand your home and make a confident offer.

Before listing, gather:

- Current property tax bill

- Recent utility costs

- Renovation invoices and warranties

- Details of furnace, air conditioner, roof, windows, and other major updates

- Survey or reference plan, if you have one

- Condo status certificate and related documents, if applicable

- Lease documents if the property is tenanted

- Permit information where available

These documents do not replace a CMA or appraisal. They support both by giving you and the buyer clearer facts about the home.

12.How Realkit Helps Keep Your Pricing and Sale Information Organized

Pricing is not a one-time guess. It is a decision you may revisit as you receive buyer feedback, compare new listings, and approach negotiations.

Realkit gives private sellers one place to keep the information that supports those decisions:

- Your listing details, upgrades, and supporting documents

- Buyer questions and showing feedback

- Offer details and counter-offer versions

- Key transaction dates once a buyer moves forward

For example, if three separate buyers mention that your price feels high relative to a recently listed home nearby, you can see that pattern rather than relying on memory. If you decide to adjust, you can update your listing information and keep a clean record of the change.

Realkit does not perform appraisals or tell you what your home is worth. It helps you run the information side of a private sale more clearly, so pricing decisions are based on an organized file rather than scattered messages and assumptions.

14.Conclusion

A CMA and an appraisal are both useful, but they answer different questions.

Use a CMA to understand your local market, compare your home with real alternatives, and choose a thoughtful listing strategy. Use a formal appraisal when you need independent valuation for a complex property, lending, an estate, separation, or another defined purpose.

For most Ontario private sellers, the best approach is not to rely blindly on either one. Build a solid pricing file, compare both sold and active homes, stay open to buyer feedback, and keep your lawyer ready once offers arrive. That gives you a much better foundation for pricing confidently without a traditional listing agent.

15.Sources

- Appraisal Institute of Canada, information for residential property owners and mortgage professionals on independent appraisals, the role of AIC-designated appraisers, and lender appraisal requirements.

- RE/MAX Canada, “Home Appraisal vs Current Market Assessment,” explaining the difference between an agent-prepared CMA and a formal lender-oriented appraisal.

- Metrix Realty, “Appraisal vs Realtor CMA: What Is the Difference in Ontario?” on CMA pricing discussions and defined appraisal assignments.

- Big Creek Realty, “Property Appraisal and Comparative Market Analysis,” explaining comparable sales, active market competition, and the different purposes of CMAs and lender appraisals.

- RFA Mortgage Corporation, “Standard Appraisal Requirements,” outlining typical mortgage appraisal expectations for comparable sales, photos, property review, and lender lending-value analysis.

- Value Trust Appraisals, FAQ guidance on independent appraisals versus market evaluations and where formal appraisals are used.